A commonly held belief among many individuals is that property prices invariably double every ten years. This notion has become a widespread mantra among prospective investors, used as a reassuring promise of the inevitable appreciation in real estate values.

It is a compelling narrative that suggests a seemingly guaranteed pathway to wealth through investing in property, pegged closely to historical rises in market values and often shared as a simple rule of thumb among enthusiasts and experts alike.

If property prices doubled every ten years – it would mean a compound annual growth rate of approximately 7%. But is this always the case? Let us delve into the facts and figures to uncover the truth behind this common misconception.

The Reality of Property Price Growth

Contrary to popular belief, property prices do not always double every decade. A study of the last four decades reveals that this phenomenon only occurred during the early-2000s boom and the first half of the 1980s. Also, the price surge during the 80s was mainly due to high inflation that affected the cost of all commodities, not just property.

In the past decade, property prices did not even outperform general inflation. Halifax, although reporting growth, clearly underlines this sub-inflation growth rate, showing average property prices up just 2.5% in January 2024 over the same time last year.

Several factors contribute to the inconsistency in property price growth.

Economy

The first and most significant is the economic climate, which is crucial in determining property values. Economic prosperity generally drives property prices up, but recessions can lead to stagnation or a price drop.

Interest rates

Additionally, changes in interest rates can heavily influence buyers’ ability to purchase homes, affecting demand and, consequently, price growth. Keeping a keen eye on interest rate trends is vital for investors looking to maximise their real estate investment returns.

Property Supply

Another factor is the supply of property. In areas where new construction does not keep pace with demand, prices likely rise. Conversely, in regions with an oversupply of homes, prices may grow more slowly or stagnate.

Government Policies

Lastly, government policies related to housing, taxes, and incentives for buyers or investors can also significantly shape the property market landscape.

However, this does not mean that investing in property is not profitable. On the contrary, you can still double your initial investment with the right strategies.

Doubling Your Investment: A Case Study

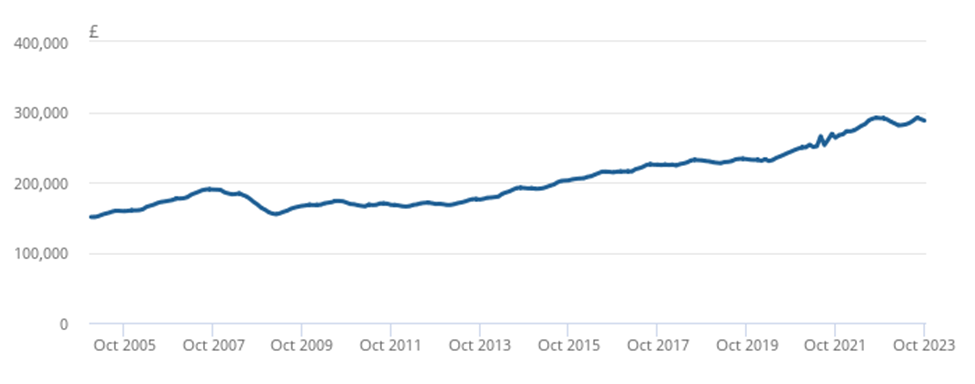

Let us consider a hypothetical scenario. Suppose you purchased an average UK home in 2013 for £175,800. You put down a 25% deposit of £43,950 of your own money and took a mortgage of £131,850. Fast forward to 2024, the same property has a value of £291,000. After selling the property and repaying the mortgage, you would have turned your initial £43,950 into £115,200.

Even when accounting for inflation, your initial £43,950 would only be worth £58,653, meaning that your property investment has almost doubled the returns from an inflation-matching savings account.

Is it really that simple?

In evaluating the real return on property investment, it is crucial to consider factors beyond inflation that can significantly impact the investment’s profitability. These include:

- Maintenance costs, property taxes, and insurance can eat into profits if not well-managed.

- Capital improvements to maintain or increase the property’s value over time.

- Potential rental income that can provide a regular cash flow but also involves management expenses and the risk of vacancy periods.

- Changes in the local real estate market and broader economic conditions can influence property values and rental rates, affecting the long-term return on the investment.

The Power of Leverage

Let us not overlook that using leverage (borrowed capital) to finance your investment can introduce additional risks. So, it is crucial to have contingency plans in place to mitigate these risks.

However, leverage can be a powerful tool when used responsibly. Even when property prices are not skyrocketing, you can still achieve impressive returns with the help of leverage.

So, for those considering mortgage borrowing for property investment this year, what can you expect?

- Firstly, expect interest rates to fluctuate, influenced by governmental and economic changes, which could significantly impact the cost of borrowing. Investors should monitor these rates closely to time their investments when borrowing costs are lower.

- Additionally, the tightening of lending criteria by banks and other financial institutions means investors must ensure their financial health is in optimal condition to qualify for the best loan terms. Make sure you have a strong credit score, a solid income history, and a low debt-to-income ratio.

- Another area to watch is the evolving landscape of government regulations, particularly those related to housing and rental markets, which can affect investment strategies and returns.

- Finally, with the ongoing uncertainty in global economies due to various factors, including ongoing conflicts, investors should remain adaptable and informed about the broader economic environment that could influence property market dynamics.

Other ‘big-picture’ aspects to keep an eye on include:

- Climate Change – Areas prone to flooding or other environmental risks may see fluctuating property values.

- Technology Advancements – These have the power to reshape industries and employment patterns. In turn, they affect where people choose to live and work.

- International Trade – New agreements and tariffs can alter economic growth rates, influencing the demand for commercial and residential properties.

- Migration Patterns – The movement of potential labour can cause demographic shifts, affecting housing demand in certain regions. Investors need to consider these global dynamics as they can have a cascading effect on local property markets.

Is property less volatile than other investments?

Over the last decade, UK property investors have experienced diverse outcomes, as have those who placed their capital in the stock market.

While both markets have their challenges and opportunities, real estate in the UK has generally offered steady capital appreciation and rental yields, especially in major cities and growth areas such as Manchester, Birmingham, and parts of London.

For example, the average house price in the UK has significantly increased, rising from around £175,000 in October 2013 to approximately £288,000 at the end of October 2023, reflecting a substantial growth (65%) in capital value.

The stock market, on the other hand, represented by indices such as the FTSE 100, has demonstrated considerable volatility influenced by global economic events including the financial crisis, Brexit, the COVID-19 pandemic, and the Ukraine conflict.

Despite these fluctuations, the stock market has also provided opportunities for high returns for investors focused on technology and green-energy sectors. For example, companies in these sectors saw their stock values multiply following the pandemic as demand for technology and sustainable solutions surged.

While UK property investors have enjoyed relatively stable growth propelled by housing demand and limited supply, stock market investors have had to navigate a more turbulent environment, with the potential for higher losses and greater gains.

In short, the appeal of investing in property or the stock market depends on an individual’s risk tolerance, investment strategy, and long-term objectives.

Key Takeaways

Property prices do not always double every 10 years. Although historical trends show this is not the case, strategic property investments can still yield significant returns. Leveraging property investments can outperform inflation and savings accounts, offering a way to grow wealth, even without doubling prices.

At Belvoir, successful property investing is not merely about riding the waves of the market. We help investors make smart, informed decisions based on thorough research and careful planning. Three key influencers to success are:

- Location and timing in real estate investments – markets can vary dramatically from city to city and even within different parts of a location. An investment that flourishes in one area might not perform as well in another due to factors like economic development, employment rates, and local amenities.

- Understanding market dynamics – alongside diligent research into future urban planning and development projects, identifying market trends can significantly enhance your investment’s potential.

- Identifying the right time to enter and exit the market – these decisions can drastically affect your investment’s outcome. By keeping a close eye on market trends and being adaptable, investors can better position themselves to capitalise on opportunities and mitigate risks.

Ready to secure your financial future through smart property investment? Consult a Belvoir Property Investment Consultant today.

Our team of experts will guide you through every step of the investment process with personalised strategies that align with your objectives. Do not miss the opportunity to make your investment goals a reality. Contact us now to start your successful property investment journey.